Traditional Reverse Mortgages: How They Work and Why a Modern Alternative May Be a Better Fit

For many Australians, the family home represents decades of financial discipline.

Over time, mortgage repayments and rising property values mean that a large portion of personal wealth becomes locked inside the property.

When goals change, unexpected expenses arise, or when retirement planning becomes more important, homeowners often look for ways to access part of their home equity without selling.

While traditional reverse mortgages are a common option, they are not the only option. And for many people, reverse mortgages may not be the most suitable solution.

What Is a Reverse Mortgage

In Australia, a reverse mortgage is a type of loan that allows you to access some of the equity in your home without making monthly repayments. This means that while interest accrues over time, the principal balance of the loan does not decrease.

Under a reverse mortgage, the original loan amount and compounding interest that has accrued over the life of the loan is generally repaid when:

- You sell the property;

- You move into aged care;

- Your estate settles the loan after you pass away; or

- You pay voluntarily.

Reverse mortgages are typically only offered to borrowers over the age of 60. Over 60s may consider reverse mortgages when they want to:

- Supplement retirement income.

- Cover unexpected or medical costs.

- Fund renovations or home modifications.

- Improve lifestyle, such as through travel or leisure.

- Refinance their existing traditional home loan.

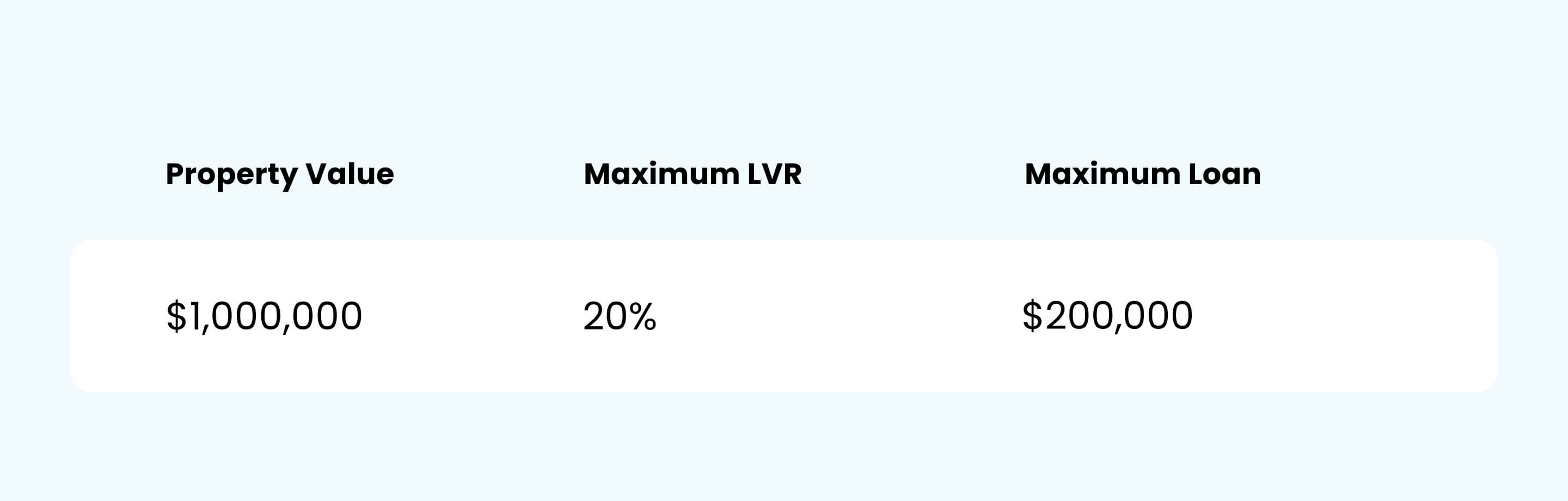

How Much Can You Borrow

Due to legislative requirements, the amount you can borrow under a reverse mortgage and how much equity you can access are determined by the age of the youngest borrower under the loan.

For example, where the youngest borrower is 60 years old, the maximum LVR permitted under a reverse mortgage will typically be 20%.

This means that if you or the youngest borrower are 60 years old, and your home is worth $1,000,000, you may only be eligible to borrow around $200,000 dollars under a traditional reverse mortgage.

Where Traditional Reverse Mortgages Can Create Challenges

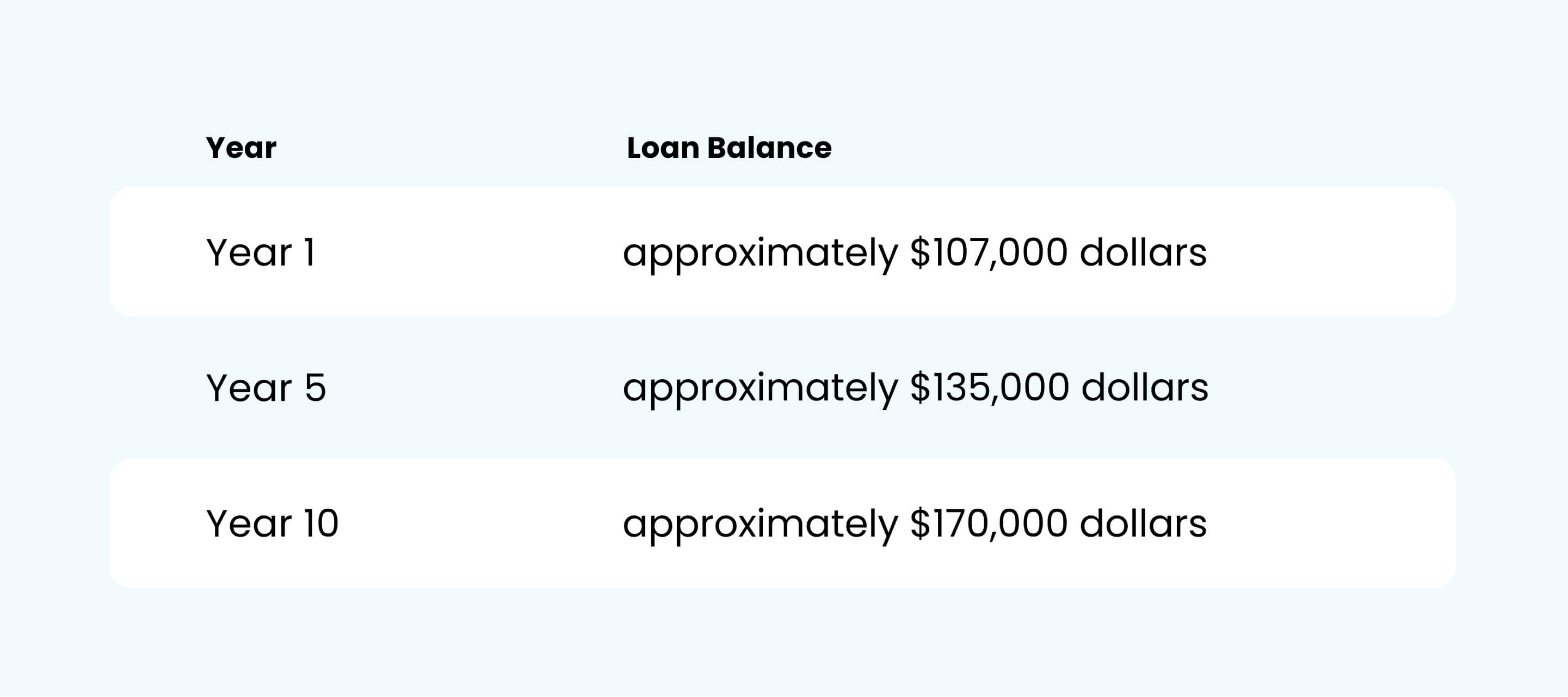

A key feature of traditional reverse mortgages is compounding interest. Compounding interest means that interest is charged on the original amount borrowed and on the interest that has already accumulated. Without regular repayments, the loan balance will increase every year because you are being charged interest on interest.

To make compounding interest clear, here is an illustrative example using a 7.00% per annum interest rate.

Please note that these calculations are an example only and included for illustrative purposes. Different loan amounts, terms, and interest rates will result in different results.

Starting loan amount $100,000 dollars. The interest rate is 7.00% per annum, compounding.

There are no monthly payments, so the outstanding loan balance increases by a greater amount each year. For some homeowners who use a traditional reverse mortgage, this becomes a concern because if the property is sold and the loan is repaid over a longer period of time, a significant part of their equity has been eroded by accumulated compounding interest.

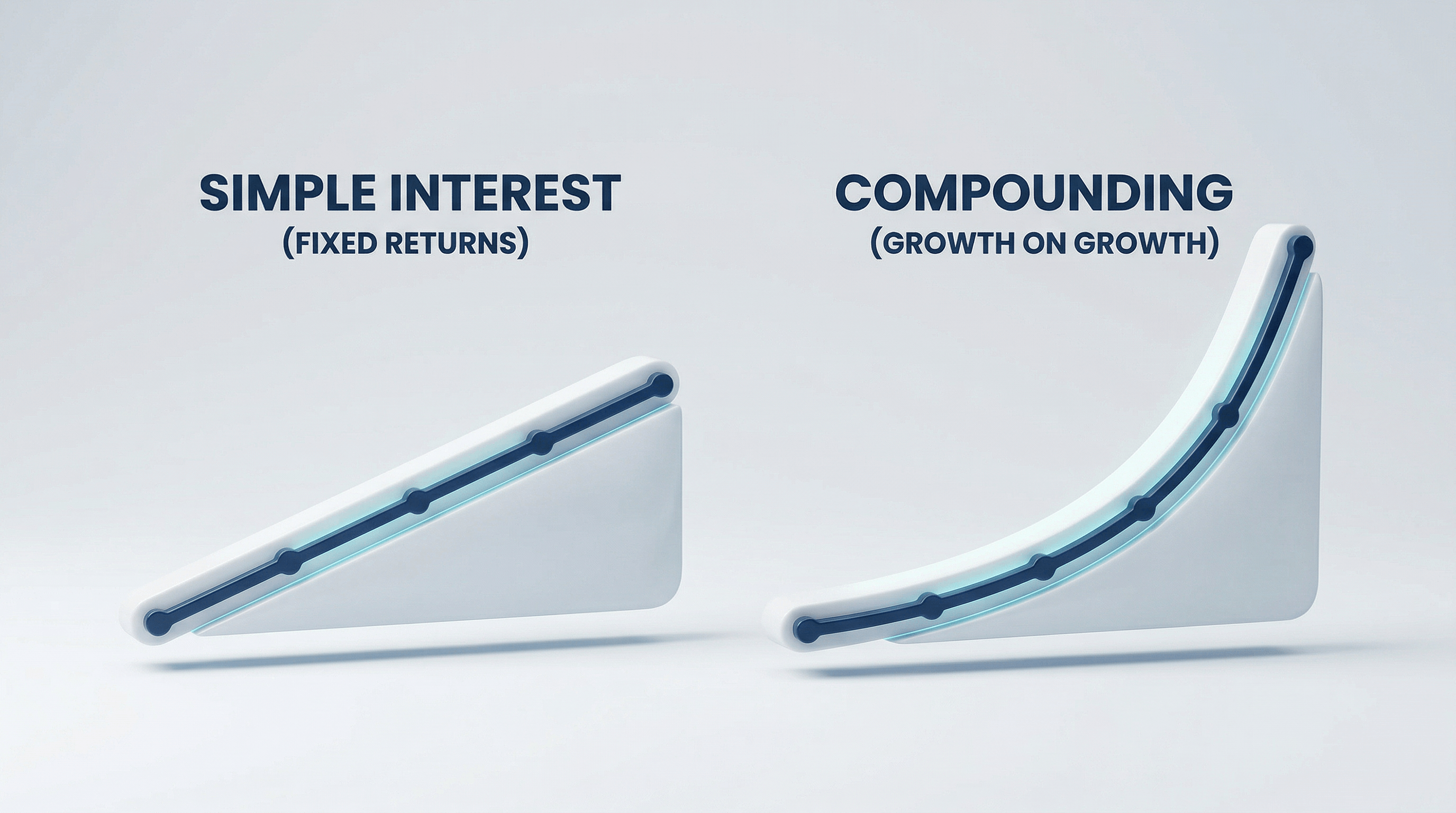

How This Differs From Simple Interest

Another type of interest is simple interest. Simple interest is only charged on the initial loan amount, irrespective of any other interest that has already accumulated over the loan.

To illustrate, here is an example using a 7.00% per annum simple interest rate where the starting loan amount is $100,000 dollars:

Please note that these calculations are an example only and included for illustrative purposes. Different loan amounts, terms, and interest rates will result in different results.

Benefits of a Traditional Reverse Mortgage

- No monthly payments.

- Access to equity without selling your home.

- Often includes flexible drawdown options if you need funds over time.

Important Considerations

- Interest compounds, which means your debt increases over time.

- Borrowing amounts can be restrictive, especially if you are younger.

- Reverse mortgages are usually only offered as a first mortgage (which will mean you must have paid off any other loans that were secured by the property).

- Generally, reverse mortgages are only available to people aged 60 and above, although legislation does permit reverse mortgage loans to persons aged 55 or above where the loan is not unsuitable.

While traditional reverse mortgages can work well for retirees who are asset rich, but cash flow limited, they can be restrictive for borrowers who need flexibility or still have income.

Situations Where a Traditional Reverse Mortgage May Have Limitations

While reverse mortgages can be useful for some retirees, they may not suit every situation.

Many homeowners may research alternatives to traditional reverse mortgages when:

- They are under the age of 60

- They still have an existing home loan they want to keep, so they require a second mortgage

- They want to reduce the amount of their monthly debt payments, by replacing existing debt with a loan that requires no monthly payments.

- Their income has temporarily reduced, such as due to starting a business, or they require long term leave, such as parental or carer’s leave

- They are not ready to retire but still want access to their home equity

- They want to avoid compounding interest and its impact on their future wealth.

If any of these situations sound familiar, there are now more flexible ways to access the equity you have built in your home.

Introducing Midkey - A Modern Alternative That Gives You Flexibility and Control

Midkey was created for homeowners who want to unlock equity without monthly payments. Midkey is Australia’s first No Monthly Payments Loan, for people in mid-life where there is no fixed repayment timeframe.

Midkey:

- Has no monthly payments.

- Has no fixed loan term or timeframe for repayment1

- Is available to homeowners aged 18 and above.

- Can be used as a first or second mortgage, which means you can keep your existing home loan.

- Uses simple interest, not compounding interest.

- Up to the age of 75, the maximum LVRs permitted under a Midkey loan are higher than a traditional reverse mortgage

Midkey includes a Deferral Fee that is only payable if your property increases in value over the life of your loan. If your home does not increase in value, no Deferral Fee applies.

You can learn more about the Midkey Deferral fee here.

Who Midkey May Suit

Midkey may be a better fit if you:

- Need access to equity during your working years.

- Have temporarily reduced income. For example, when you are starting a business, or when you require long-term leave, such as parental or carer’s leave.

- Want to reduce the amount of your monthly debt payments by replacing your existing debt (e.g., home loan, credit card, ATO) with a loan that requires no monthly payments.

- Want to support children in buying a property.

- Want to renovate or buy a bigger home.

- Want flexibility without the pressure of monthly payments.

- Require all of your loan proceeds immediately.

The Bottom Line

Traditional reverse mortgages have historically been the primary way for the over-60s to release equity without selling. But they typically come with compounding interest, age restrictions, and rigid rules around borrowing. Today, homeowners have more choice.

Midkey gives you a modern way to unlock equity on your terms.

- No monthly payments.

- Simple interest, not compounding.

- No requirement to be over 60.

Ready to see if Midkey could work for you?

You can check your eligibility in under 2 minutes.

There is no obligation and no impact on your credit score.

This article has been prepared by Midkey and contains general information only. It is not intended to be relied on as advice. It does not take into account your objectives, financial situation or needs. Before acting on any information in this article, you should consider whether it is appropriate for your circumstances. Midkey recommends you that you seek independent legal, property, financial, or taxation advice before acting on any information in this article.

References

1 Repayment triggers for Midkey loans are included in your contract. The loan will need to be repaid if you die, you move into an aged care facility, or the LVR exceeds 100%.